Buying a home is one of the biggest financial decisions for Indian families. For most buyers, this decision is closely linked to home loan interest rates, monthly EMIs, and long-term repayment comfort. In 2026, borrowers are closely tracking changes in SBI home loan interest rates due to evolving RBI policies and market conditions.

State Bank of India remains the largest home loan lender in India, and its interest rates often act as a benchmark for the entire housing loan market. This article explains SBI home loan interest rates in 2026 in a simple, practical, and decision-focused manner.

Index

- Why SBI Home Loan Interest Rates Matter in 2026

- What Is the SBI Home Loan Interest Rate in 2026?

- How SBI Home Loan Interest Rates Are Calculated

- SBI Home Loan Interest Rates Based on CIBIL Score 2026

- Types of SBI Home Loans and Their Interest Rates

- SBI Home Loan Processing Fees and Other Charges

- Eligibility Criteria for SBI Home Loans

- Documents Required for SBI Home Loan

- EMI Impact: How Interest Rates Affect Your Monthly Payment

- SBI vs Other Banks: Interest Rate Comparison 2026

- Advantages of SBI Home Loans

- Limitations to Keep in Mind

- Using EMI and Eligibility Calculators

- Final Expert View

- Frequently Asked Questions (FAQs)

Why SBI Home Loan Interest Rates Matter in 2026

Home loan interest rates directly affect:

- Your monthly EMI

- Total interest paid over 20-30 years

- Eligibility for a higher or lower loan amount

- Long-term financial stability

In 2026, interest rates are especially important because most SBI home loans are linked to repo rate based external benchmarks. This means even small RBI rate changes can impact your EMI.

For first-time buyers, understanding how SBI decides interest rates helps avoid confusion and unrealistic expectations.

What Is the SBI Home Loan Interest Rate in 2026?

As of 2026, SBI home loan interest rates generally range between:

7.50% to 8.70% per annum

The exact rate offered to a borrower depends on multiple factors such as credit score, loan type, and risk profile.

Key Highlights at a Glance

| Particulars | Details |

|---|---|

| Interest Rate Range | 7.50% – 8.70% p.a. |

| Benchmark | Repo-linked EBLR |

| Maximum Tenure | Up to 30 years |

| Prepayment Charges | Nil |

| Processing Fee | 0.35% + GST (min ₹2,000, max ₹10,000) |

How SBI Home Loan Interest Rates Are Calculated

Repo-Linked External Benchmark (EBLR)

SBI home loans are linked to the External Benchmark Lending Rate (EBLR), which is derived from:

RBI Repo Rate + Bank Spread

For example:

- RBI Repo Rate: 5.50%

- SBI Spread: 2.65%

- EBLR: 8.15%

Your final interest rate is EBLR plus or minus a risk-based adjustment depending on your credit profile.

Why This Matters for Borrowers

- EMI can increase or decrease automatically when RBI changes repo rates

- Transparency is higher compared to older MCLR-based loans

- Rate transmission is faster

SBI Home Loan Interest Rates Based on CIBIL Score 2026

Your CIBIL score plays a crucial role in determining your interest rate.

| CIBIL Score | Applicable Interest Rate |

|---|---|

| 800 and above | 8.15% |

| 750 – 799 | 8.25% |

| 700 – 749 | 8.35% |

| 650 – 699 | 8.45% |

| 550 – 649 | 8.65% |

| New to credit / No score | 8.35% |

For a detailed explanation on how CIBIL score impacts SBI home loan interest rates and how to improve your eligibility, check our complete guide → SBI Home Loan Interest Rates Based on CIBIL Score 2026

Types of SBI Home Loans and Their Interest Rates

SBI offers multiple home loan variants designed for different borrower needs.

| Loan Type | Interest Rate Range |

|---|---|

| Regular Home Loan | 7.50% – 8.70% |

| Maxgain (Overdraft) | 7.75% – 8.95% |

| Top-Up Loan | 8.00% – 10.75% |

| Top-Up (OD) | 8.25% – 9.45% |

| Loan Against Property | 9.20% – 10.75% |

| Reverse Mortgage | 10.55% |

| YONO Insta Top-Up | 8.35% |

Each SBI home loan variant suits different needs. Detailed comparisons and use-cases are explained separately.

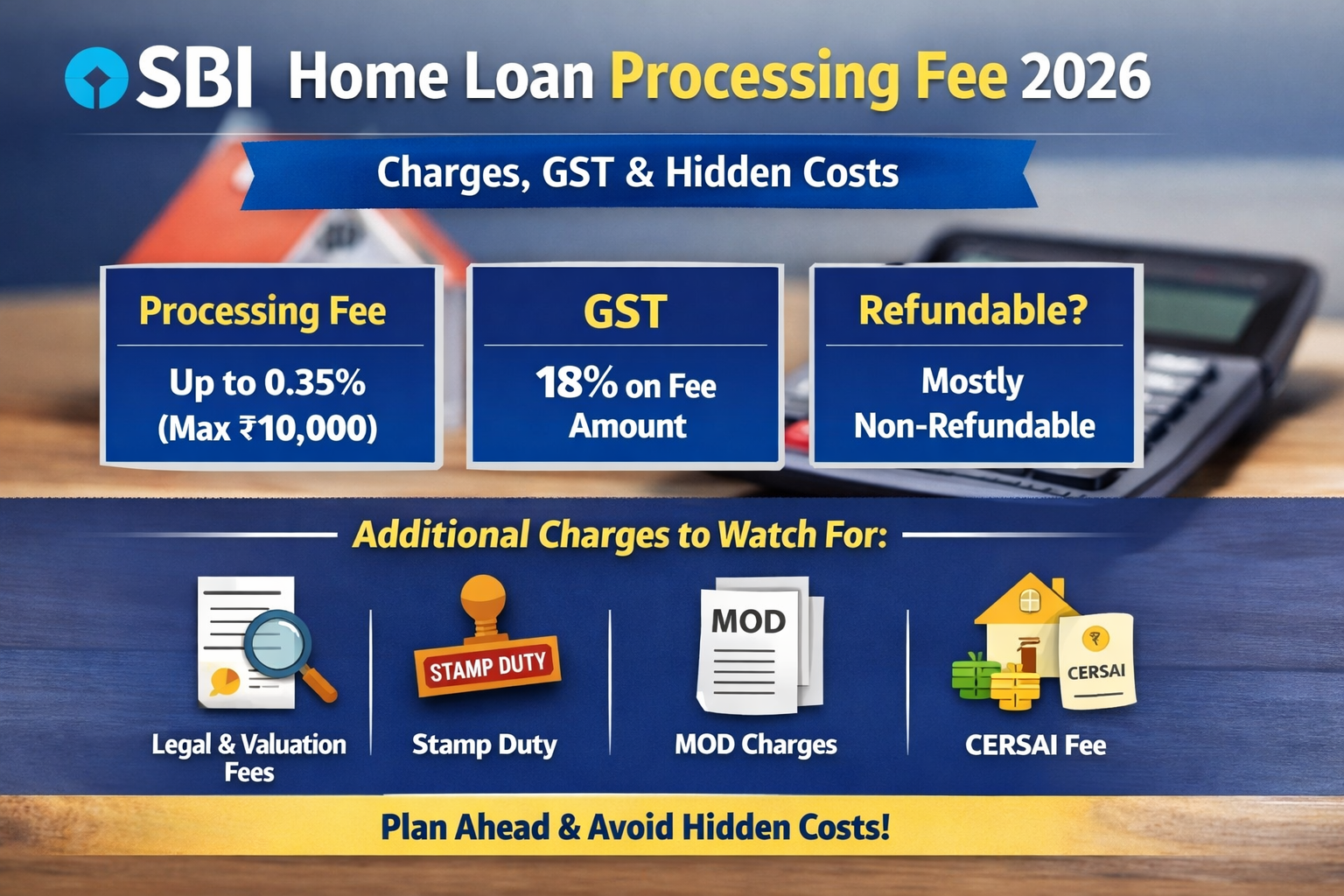

SBI Home Loan Processing Fees and Other Charges

Processing Fee

- 0.35% of loan amount + GST

- Minimum: ₹2,000 + GST

- Maximum: ₹10,000 + GST

Other Charges

- Legal and valuation charges (often bundled)

- No foreclosure or prepayment penalty on floating-rate loans

Read the complete breakdown of SBI home loan processing fees, legal charges, and hidden costs here → SBI Home Loan Processing Fee 2026

{kind=link}

Eligibility Criteria for SBI Home Loans

To apply for an SBI home loan in 2026, you generally need to meet the following criteria:

- Residency: Resident Indian (NRIs have separate schemes)

- Age: 18 to 70 years

- Employment: Salaried or self-employed

- Tenure: Up to 30 years (subject to age)

Eligibility also depends on income stability, repayment capacity, and existing liabilities.

Documents Required for SBI Home Loan

Common Documents

- Identity proof (PAN, Aadhaar, Passport)

- Address proof

- Income documents (salary slips / ITRs)

- Bank statements (last 6 months)

- Property documents (agreement, approvals, OC)

View the complete SBI home loan document checklist here → Documents Required for SBI Home Loan 2026 – Full Checklist

EMI Impact: How Interest Rates Affect Your Monthly Payment

Even a small rate change affects EMIs significantly.

Example:

- Loan Amount: ₹50 lakh

- Tenure: 25 years

| Interest Rate | Approx EMI |

|---|---|

| 8.15% | ₹39,200 |

| 8.45% | ₹40,200 |

A 0.30% increase raises EMI by ~₹1,000 per month and adds several lakhs in interest over time.

You can calculate your exact EMI using our SBI home loan EMI calculator based on loan amount, tenure, and interest rate.

SBI vs Other Banks: Interest Rate Comparison 2026

| Bank | Interest Rate Range |

|---|---|

| SBI | 7.50% – 8.70% |

| Bank of Baroda | 7.45% – 9.20% |

| Axis Bank | 8.35% – 9.35% |

| HDFC Bank | 7.90% – 13.20% |

| ICICI Bank | 8.75% – 9.80% |

Rates should not be the only comparison factor. Processing transparency, prepayment rules, and long-term stability also matter.

Advantages of SBI Home Loans

- Competitive interest rates

- Zero foreclosure charges

- Long repayment tenure

- Strong legal due diligence

- Wide branch network

Limitations to Keep in Mind

- Documentation process can be time-consuming

- Approval timelines may vary by branch

- OD-based products may not suit all borrowers

Understanding these limitations helps set realistic expectations.

Using EMI and Eligibility Calculators

Before applying, borrowers should use home loan calculators to:

- Estimate EMI comfortably

- Understand affordability

- Compare tenure options

- Plan prepayments

These tools reduce guesswork and prevent over-borrowing.

Final Expert View

SBI home loan interest rates in 2026 remain among the most competitive in the Indian market, especially for borrowers with strong credit profiles. The repo-linked structure ensures transparency, while zero prepayment charges provide long-term flexibility.

However, borrowers should focus not just on the lowest rate but also on repayment comfort, income stability, and future financial goals. SBI home loans are best suited for borrowers seeking stability, transparency, and long-term trust.

Frequently Asked Questions (FAQs)

1. What is the minimum SBI home loan interest rate in 2026?

The minimum interest rate starts from around 7.50% per annum, subject to credit profile.

2. Is SBI home loan interest rate fixed or floating?

SBI offers mainly floating-rate loans linked to the repo rate.

3. Does SBI charge prepayment penalty?

No, SBI does not charge any prepayment or foreclosure penalty on floating-rate home loans.

4. How does CIBIL score affect SBI home loan rates?

Higher CIBIL scores attract lower interest rates and faster approvals.

5. Can SBI home loan EMI change during tenure?

Yes. Since loans are repo-linked, EMIs can change when RBI revises repo rates.

6. Is SBI good for long-term home loans?

Yes. SBI is considered suitable for long tenures due to stable policies and no foreclosure charges.

7. Can self-employed individuals apply for SBI home loans?

Yes, SBI offers home loans to both salaried and self-employed applicants.